Public consultation on transfer pricing matters (19-20 March 2015)

The OECD will hold a public consultation event on transfer pricing matters on 19-20 March 2015 at the OECD Conference Centre in Paris, France.

Public comments received on discussion drafts of two new elements of the OECD International VAT/GST Guidelines

On 18 December 2014, the OECD invited comments from interested parties on discussion drafts of two new elements of the OECD International VAT/GST Guidelines. These discussion drafts related to (i) the place of taxation of business-to-consumer supplies of services and intangibles (B2C Guidelines) and (ii) provisions to support the application of the Guidelines in practice (Supporting provisions)

Public Consultation: Interest Deductions and other financial payments

A public consultation on BEPS Action Item 4 (Interest deductions and other financial payments) was held in Paris at the OECD Conference Centre on 17 February 2015.

Public comments received on discussion draft on Action 4 (Interest Deductions and Other Financial Payments) of the BEPS Action Plan

On 18 December 2014, interested parties were invited to comment on the discussion draft on Action 4 (Interest Deductions and other Financial Payments) of the BEPS Action Plan. The OECD is grateful to the commentators for their input and now publishes the comments received.

Public comments received on discussion draft on the transfer pricing aspects of cross-border commodity transactions (BEPS Action 10)

On 16 December 2014, the OECD invited comments from interested parties on a discussion draft on the transfer pricing aspects of cross-border commodity transactions. This work relates to Action 10 of the BEPS Action Plan. The OECD is grateful to the commentators for their input, and now publishes the comments received.

Public comments received on the discussion draft on the use of profit splits in the context of global value chains (BEPS Action 10)

On 16 December 2014, the OECD invited comments from interested parties on a discussion draft on the use of profit splits in the context of global value chains. This work relates to Action 10 of the BEPS Action Plan. The OECD is grateful to the commentators for their input, and now publishes the comments received.

Public comments received on discussion draft on Actions 8, 9 and 10 : revisions to Chapter I of the Transfer Pricing Guidelines (Including risk, recharacterisation and special measures) of the BEPS Action Plan

On 19 December 2014, interested parties were invited to comment on the discussion draft on Actions 8, 9 and 10: revisions to Chapter I of the Transfer Pricing Guidelines (Including risk, recharacterisation and special measures) of the BEPS Action Plan. The OECD is grateful to the commentators for their input and now publishes the comments received.

Public Consultation: Make dispute resolution mechanisms more effective

A public consultation on BEPS Action 14 (Make dispute resolution mechanisms more effective) is scheduled to be held in Paris at the OECD Conference Centre on 23 January 2015.

Public comments received on discussion draft on Action 14 (Make dispute resolution mechanisms more effective) of the BEPS Action Plan

On 18 December 2014, the OECD invited comments from interested parties on the discussion draft on Action 14 (Make dispute resolution mechanisms more effective) of the BEPS Action Plan. The OECD now publishes the comments received.

Public comments received on follow-up work on Action 6 (Prevent treaty abuse) of the BEPS Action Plan

On 21 November 2014, the OECD invited comments from interested parties on the discussion draft on Action 6 (Prevent treaty abuse) of the BEPS Action Plan. The OECD now publishes the comments received.

Public comments received on discussion draft on Action 7 (Prevent the Artificial Avoidance of PE Status) of the BEPS Action Plan

On 31 October 2014, the OECD invited comments from interested parties on the discussion draft on Action 7 (Prevent the Artificial Avoidance of PE Status) of the BEPS Action Plan. The OECD now publishes the comments received.

Release of discussion draft on revisions to Chapter I of the Transfer Pricing Guidelines (Including risk, recharacterisation and special measures)

Public comments are invited on this discussion draft which deals with work in relation to Actions 8,9, and 10 of the Action Plan on Base Erosion and Profit Shifting (BEPS).

Release of a discussion draft on Action 14 (Make dispute resolution mechanisms more effective) of the BEPS Action Plan

Public comments are invited on a discussion draft which deals with the work on Action 14 (“Make dispute resolution mechanisms more effective”) of the BEPS Action Plan.

Release of a discussion draft on Action 4 (Interest deductions and other financial payments)

Public comments are invited on a discussion draft which deals with action 4 (Interest deductions and other financial payments) of the BEPS Action Plan

Release of discussion draft on the transfer pricing aspects of cross-border commodity transactions

Public comments are invited on the discussion draft on the Transfer Pricing aspects of cross-border Commodity transactions released as part of the OECD Centre for Tax Policy's work on Action 10 of the Action Plan on Base Erosion and Profit Shifting.

Release of discussion draft on the use of profit splits in the context of global value chains as part of the work on BEPS Action 10

Public comments are invited on the discussion draft on the use of profit splits in the context of global value chains, released as part of the work in relation to Action 10 of the BEPS Action Plan.

Release of a discussion draft on follow-up work on Action 6 (Prevent treaty abuse) of the BEPS Action Plan

Public comments are invited on a discussion draft which deals with follow-up work mandated by the Report on Action 6 (“Prevent the granting of treaty benefits in inappropriate circumstances”) of the BEPS Action Plan.

Public comments received on the Paper on Transfer Pricing Comparability Data and Developing Countries

This page shows a full table of comments received from the public on the Interim Draft Paper on Transfer Pricing Comparability Data and Developing Countries.

OECD releases public request for input on BEPS Action 11

Public comments are invited on request for input on BEPS Action 11 regarding work on establishing methodologies to collect and analyse data on BEPS and the actions to address it.

Public consultation on transfer pricing documentation and country-by-country reporting

The OECD will hold a public consultation on the discussion draft on transfer pricing documentation and country-by-country reporting on 19 May 2014 at the OECD in Paris, France.

Public comments received on discussion draft on Action 6 (Prevent Treaty Abuse) of the BEPS Action Plan

The OECD publishes comments received from interested parties on the discussion draft on Action 6 (Prevent Treaty Abuse) of the BEPS Action Plan.

Release of discussion draft on Action 1 (Tax Challenges of the Digital Economy) of the BEPS Action Plan

Public comments are invited on a discussion draft that includes the proposals produced with respect to Action 1 (Tax Challenges of the Digital Economy) of the BEPS Action Plan.

Release of discussion drafts on Action 2 (Neutralise the effects of hybrid mismatch arrangements) of the BEPS Action Plan

Public comments are invited on discussion drafts that include the proposals produced with respect to Action 2 (Hybrid Mismatch Arrangements) of the BEPS Action Plan.

Release of discussion draft on Action 6 (Prevent Treaty Abuse) of the BEPS Action Plan

Public comments are invited on a discussion draft that includes the proposals produced with respect to Action 6 (Prevent Treaty Abuse) of the BEPS Action Plan.

Public comments on new draft elements of the OECD International VAT/GST Guidelines are published

Following the recent invitations for public comment on four new draft elements of the OECD International VAT/GST Guidelines, the OECD has now published the comments received which will be used to inform the OECD’s work in this area.

Public comments received on the revised discussion draft on the definition of “permanent establishment” (Article 5) of the OECD Model Tax Convention

On 19 October 2012, the OECD Committee on Fiscal Affairs released for public comment a revised discussion draft on the definition of “permanent establishment” (Article 5) of the OECD Model Tax Convention. The OECD has now published the comments received on this revised discussion draft.

Public comments received on the revised discussion draft on tax treaty issues related to emissions permits and credits

On 19 October 2012, the OECD Committee on Fiscal Affairs released for public comment a revised discussion draft on tax treaty issues related to emissions permits and credits. The OECD has now published the comments received on this revised discussion draft.

Public comments received on the revised proposals concerning the meaning of “beneficial owner” in Articles 10, 11 and 12 of the OECD Model Tax Convention

On 19 October 2012, the OECD Committee on Fiscal Affairs released for public comment revised proposals concerning the meaning of “beneficial owner” in Articles 10, 11 and 12 of the OECD Model Tax Convention. The OECD has now published the comments received on this revised discussion draft.

Public comments received on the discussion draft on the definition of “permanent establishment” in the OECD Model Tax Convention

Public comments received on the proposed changes to the Commentary on Article 5 (Permanent Establishment) of the OECD Model Tax Convention.

Post-crisis debt overhang: Growth implications across countries

Public debt in the OECD area passed annual GDP in 2011 and is still rising. This paper was prepared for the Reserve Bank of India Second International Research Conference 2012: “Monetary Policy, Sovereign Debt and Financial Stability: The New Trilemma”, 1-2 February, 2012 in Mumbai, India

Public comments received on the discussion draft on the meaning of “beneficial owner” in the OECD Model Tax Convention

Public comments received on the discussion draft on the meaning of “beneficial owner” in the OECD Model Tax Convention

Public and private actors: All on Board for Inclusive Growth

To tackle rising inequalities we need to reassess the way in which our economies grow. By placing inclusiveness at the heart of the growth debate we can open up opportunity so that every citizen can realise their potential, to contribute to, and benefit from, more equitable economic growth, said OECD Secretary-General.

Public Relations,Internet Promotion

Company: TFG Digital India

Experience: 0 to 3

Salary: 3.50 to 6.50

location: Bengaluru / Bangalore, Kolkata

Ref: 24812629

Summary: An opportunity for Part Time Work From Home. Candidates with the profile of Digital marketing, Online Promotion or Business Development can also apply for this.

Publication Writer

Company: Golden Opportunities Private Limited

Experience: 4 to 7

location: Noida

Ref: 24738584

Summary: Description

Publication Writer Job Description: Development & review of manuscripts, review articles, posters, abstracts, encore abstracts, letters to editors of Medical journals etc. Manage the project of respective....

Public Cloud Services In India To Reach $1.3 Bn In 2016: Gartner

The public Cloud services market in India will grow 35.9 pct in 2016 to total $1.3 billion, a new report by market research firm Gartner revealed on Friday.

Public Health Strategies Can Use Low/no Calorie Sweeteners

Low/no-calorie sweeteners can make a massive impact on public health strategies and may curb diabetes and increase health awareness. all of them have

Public health directors in England are asked to take charge of Covid-19 testing

Care minister’s request is admission that centralised programmes have fallen short

Ministers have asked local directors of public health to take charge of Covid-19 testing in English care homes in what will be seen as a tacit admission that centralised attempts to run the programme have fallen short.

In a letter to sector leaders, seen by the Guardian, the care minister, Helen Whately, acknowledged that testing of care home residents and staff needs to be “more joined up”. She describes the new arrangements as “a significant change”.

Continue reading...

Publisher Alerts: Complaints at Month9 Books, Nonstandard Business Practices at Black Rose Writing

In mid-2016, I wrote about YA publisher Month9 Books' abrupt decision to scale back its list, reverting rights to as many as 50 authors across all its imprints. Explaining the culling, Month9 founder and CEO Georgia McBride cited her own health problems, along with staffing issues and the company's "substantial growing pains" over the past six to nine months.

McBride's announcement triggered a surge of complaints from Month9 authors, who described a host of serious problems at the company, including late or missing payments (for staff as well as authors), problems with royalty accounting, delayed pub dates, broken marketing promises, overcrowded publication schedules, communications breakdowns, and harsh treatment and bullying by McBride.

According to authors and staff, these problems were not new or even recent, but had been ongoing for a long time. Why had authors kept silent? Almost every writer who contacted me mentioned their fear of retaliation--along with the draconian NDA included in Month9's contracts. I've rarely encountered a situation where authors seemed so fearful of their publisher.

Things quieted down after the initial flood of revelations, as they often do. Month9 survived and kept on publishing, though its list continued to shrink: between a high point in 2016 and now, the number of titles appears to have fallen about 50%. Apart from a handful of additional complaints in late 2016 and early 2017 (similar to this one), I didn't hear much about Month9 in the years following.

Until now. Over the past few weeks, I've been contacted by multiple writers who say they are still suffering from the same problems that surfaced in 2016: primarily, late (sometimes very late) royalty and subrights advance payments and statements (in many cases received only after persistent prodding by authors and their agents), and allegations of irregularities in royalty reporting.

The intimidation level, too, seems not to have changed. Most of the authors told me that they feared reprisal for coming forward, and asked me specifically not to mention their names or book titles. (Writer Beware never reveals names or other unique identifying information, unless we receive specific permission from the individual. That disclaimer is included on our website and in our correspondence.)

If you've been following the recent ChiZine scandal, you may be feeling some deja vu--notably, in the alleged existence of a toxic culture within the publisher that makes authors fearful and and helps to keep them silent. It's disappointing to learn that even if the issues that thrust Month9 into the spotlight three years ago have gone quiet, they don't seem to have eased. Writers be warned.

I wrote about Black Rose Writing in 2009, in connection with its requirement that authors buy their own books. Writers who submitted were asked how many of their own books they planned to buy; their response was then written into their contracts. (Book purchase requirements are back-end vanity publishing: even if writers aren't being asked to pay for production and distribution, they still must hand over money in order to see their work in print.)

Black Rose got rid of the book purchase requirement a few years later, and claimed to be a completely fee-free publisher. I had my suspicions that money might still somehow be involved, though...and as it turns out, I wasn't wrong.

I've recently learned that new Black Rose authors receive a Cooperative Marketing Catalog that sells a range of pay-to-play marketing and promotional services, with costs ranging from a few hundred dollars to four figures. For instance:

It's true that purchase is optional (though I would guess that authors are heavily solicited to buy). But reputable publishers don't sell marketing services to their authors--and in any case, much of what's on offer are things that other publishers, even very small ones, do for their authors free of charge, as part of the publication process.

That's not the only way in which Black Rose authors are encouraged to pay their publisher. Owner Reagan Rothe is a self-described "financial partner" in two additional businesses: the Maxy Awards, a high entry fee book competition that donates "a large part of every entry" to a charity (how large? No idea; that information is not provided); and Sublime Book Review, a paid review service.

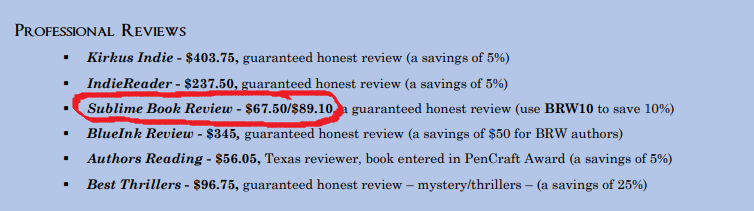

Though Mr. Rothe's financial interest in these businesses is not disclosed on the business's websites, both businesses are clearly energetically promoted to Black Rose authors. On Sublime's website, nineteen of the first 20 book reviews are for Black Rose books. There's also this, from the marketing catalog (note the lack of disclaimer):

As for the Maxys, thirteen of the 17 winners and runners-up for 2019 are Black Rose books.

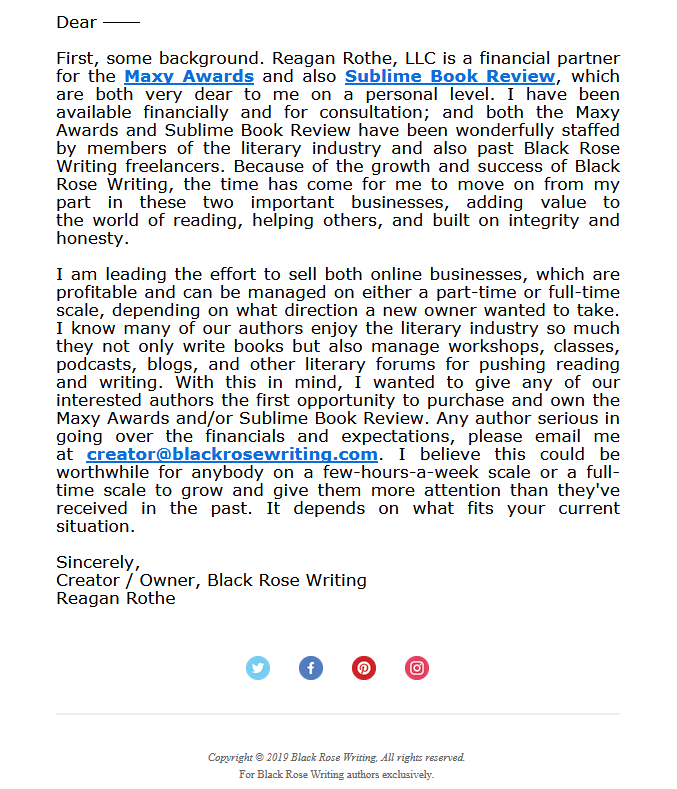

Mr. Rothe does admit his relationship with the businesses in this recent email to Black Rose authors--though only to afford them yet another opportunity to give him money:

public bathroom mouthwash

The Worst Things For Sale is Drew's blog. It updates every day. Subscribe to the Worst Things For Sale RSS!

public service announcement

The Worst Things For Sale is Drew's blog. It updates every day. Subscribe to the Worst Things For Sale RSS!

pube store

HOLY SHIT WE DID IT!!! Superpoop is back and updates every Thursday. Drewtoothpaste is back and updates every Monday. Subscribe to the combined RSS feed for Superpoop and Drewtoothpaste and get updates in your RSS reader.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}